Careful estate tax planning maximizes the legacy you leave for the next generation and minimizes the transaction costs of administration and asset transfers, and when planning concerns high net worth estates, tax planning becomes critical. With substantial tax exemption changes on the horizon, there is now an even greater sense of urgency to take advantage of current laws to minimize federal estate taxes, gift taxes and generation-skipping transfer taxes. This article will focus on an overview of some of the basic strategies and a follow up will expand with additional strategies using a number of irrevocable trusts such as SLAT Trusts, GRATs, GRUTS, as well as GST Trusts. For now, let’s look at basic estate tax planning and A-B Trusts for high net worth estates as a foundation.

Potential Federal Estate Tax Changes

High Net Worth Estate Planning in Florida and A-B Trusts

When it comes to estate tax planning and A-B Trusts, high net worth estates in particular, raise special planning goals like long-term preservation of family heirloom assets, deterrence of squandering, and – of course – reduction of estate-tax liability. And as of this writing, substantial federal tax law changes that will, if enacted, impact many more high net worth estates are looming on the horizon.

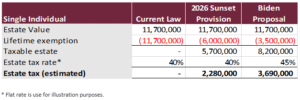

Under current (2021) rules, only estates valued at $11.7 million or more qualify for federal estate taxes. But for those that qualify, the rates go as high as 40%. Thirteen states and Washington, D.C., add estate taxes at the state level. Florida, however, is not among them – just one of the reasons Florida is a great jurisdiction to plan a high-net-worth estate.

Not only does Florida’s state government not impose any income, estate, inheritance, or gift taxes, but state law also recognizes most forms of joint ownership (e.g., POD and TOD designations, joint tenancy, tenancy by the entireties) that allow assets to pass outside of probate with minimal transaction costs. Even more, Florida’s version of the Rule Against Perpetuities permits dynasty trusts to endure for over 300 years, or all but indefinitely. All told, Florida’s estate-friendly legal climate affords planners an impressive assortment of Florida wealth-transfer options to choose from.

Most high-net-worth estate plans in Florida rely on some combination of strategic gifts, trusts, and wills. In practice, the three frequently work symbiotically. For instance, gifts might be used to fund a trust in Florida. Or, a last will & testament in Florida might create one or more testamentary trusts. A testamentary trust in Florida is a trust declared in a will and funded using assets that pass through probate, allowing the testator to leave instructions for use of assets after death, while retaining control during life. A living trust, on the other hand, is a revocable inter vivos (“during life”) trust in Florida that can accomplish many of the same objectives as a will, but without the need for probate.

Living trusts are sometimes touted as a will replacement to be used instead of a separate will. While this is occasionally possible, it is often a false choice. Many estates, especially high-net-worth estates, are best served with a will in place, even if it’s just a pour-over will acting as a safeguard in case any assets aren’t otherwise accounted for.

There are literally scores of specialized estate-planning strategies available in Florida. The usefulness of each depends upon your individual goals, financial situation, and family status. A few approaches have proven particularly effective for affluent estates, but these are by no means the only options.

Strategic Gifting in Florida

It seems like an obvious solution if you want to reduce estate taxes, why not just give some of your wealth to your heirs before you die, right? Well, yes…but there’s a catch. The IRS also charges a gift tax for gifting strategies in Florida and elsewhere. Like the estate tax, the gift tax is subject to an exemption. Where it gets tricky is that the gift tax and estate tax exemptions are essentially the same exemption, so every dollar of gift tax exemption you claim during life is one fewer estate-tax-exemption dollar available upon death. However, the gift tax also has a $15,000 annual exclusion per recipient, so the tax only applies to the extent you gift a single recipient more than $15,000 in value in a single year. Thus, you can transfer up to $15,000 per year to each of your children without paying gift tax or eating into your estate tax exemption. And married couples can combine their annual exclusions, allowing up to $30,000 per year, per child (or another recipient). Repeat over a few years, and you can remove a lot of wealth from your estate tax-free.

Using a Crummey Trust in Florida

A Crummey Trust uses the annual gift tax exclusion to fund an irrevocable trust. The grantor of the trust gets to decide in advance how trust assets are used but cannot exercise any control after funding (that’s the trustee’s job). The benefits are that assets transferred to a Crummey Trust are removed from the eventual taxable estate, and the trust avoids any estate tax on growth that accrues from the time of funding to the time of death. To be effective, though, the trust’s beneficiary must be allowed a limited period to access the assets when transferred to the trust. A beneficiary who doesn’t cooperate defeats the purpose of the trust. This type of trust is also commonly known as an ILIT which is discussed in more detail to follow.

Irrevocable Life Insurance Trusts (ILIT) in Florida

An irrevocable life insurance trust (ILIT) in Florida is created to be the legal owner and beneficiary of a life insurance policy used for estate planning purposes in Florida and elsewhere so that the policy’s value is not part of the eventual taxable estate. During life, you gift the policy’s premium payments to the trust for the trustee to pay to the insurance company. Upon death, the policy pays out to the trust, and the trustee distributes the proceeds according to directions set forth in the instrument creating the trust. ILITs are commonly used as a source of liquidity to pay estate or other taxes due on illiquid assets, like real estate.

Generation-Skipping Trusts in Florida

Also called “dynasty trusts,” generation-skipping trusts in Florida and elsewhere are designed to avoid cumulative estate taxes over multiple generations. Once wealth is in the trust and either the generation-skipping tax (“GST,” a tax on transfers that skip a generation) is paid or the GST exemption is used, the wealth will not be subject to estate taxes again as long as it stays in the trust. This GST Trust planning strategy is particularly powerful in a time where existing exemption amounts are scheduled to decrease. The trust instrument can designate succeeding generations as beneficiaries or empower the trustee to appoint new beneficiaries in the future. Dynasty trusts ensure that assets continue to benefit the family over multiple generations, protect wealth in the trust from squandering or creditor claims, and avoid loss in a beneficiary’s later divorce. Florida’s extended Rule against Perpetuities allows dynasty trusts in Florida to remain effective for over 300 years if not earlier terminated by their own terms.

Family Limited Partnerships or LLCs in Florida

A family limited partnership or LLC in Florida is a corporate entity created to hold family assets. Rather than transfer wealth directly to subsequent generations, the older generation gifts ownership interests in the entity, while retaining managerial control. Because the gifted interests do not have management rights, they are deemed to have a reduced value – up to 40% less than the corresponding asset value. Thus, a gift of ownership interests calculated to equal the $15,000 annual gift tax exclusion can effectively transfer considerably more wealth without triggering the gift tax.

Qualified Personal Residence Trusts (QPRT) in Florida

A QPRT is an irrevocable trust created to hold title to the grantor’s residential real estate. When transferring the property, the deed reserves the right to continue living in the home for a defined period, after which the trust typically holds title in fee simple. The instrument creating the QPRT declares how the property is to be used or distributed by the trustee at the end of the term. Because the trust is irrevocable, the value of the residence is removed from the taxable estate.

Using A-B Trusts (a/k/a Bypass Trust) for High Net Worth Estates in Florida

We saved the question of estate tax planning and A-B Trusts for high net worth estates because these trusts have historically experienced many changes and are now snapping back from one extreme (not being very important) to the other (again becoming a critical planning option). But before getting into that, we need to establish what an A-B trust is.

The idea behind A-B trusts is for spouses to reduce or eliminate estate taxes by taking full advantage of the unlimited spousal exemption and both spouses’ lifetime exemptions. When one spouse dies, the tax code allows him or her, through the unlimited spousal exemption, to transfer all wealth to the surviving spouse with no estate tax liability. The problem, historically, was that, when the second spouse died, the estate would be taxed on all wealth exceeding the second spouse’s exemption. So, the first spouse’s exemption was essentially wasted. Enter the A-B trust.

An A-B trust is actually two complementary trusts created through a will or living trust. Upon the death of the first spouse (“Husband”), the A Trust (or “marital trust”) is funded with all assets exceeding the value of Husband’s exemption. The A Trust is exempt from estate taxes under the spousal exemption because the surviving spouse (“Wife”) is the beneficiary. At the same time, the B Trust (or “bypass trust”) is funded up to the amount of Husband’s exemption. B Trust can be used to support Wife, but Wife cannot have any ownership interest or control over the assets. Upon Wife’s death, the wealth in both trusts passes to other designated beneficiaries. The value of assets in the A Trust is subject to estate taxes after applying Wife’s exemption, but the B Trust is not included within Wife’s estate.

The utility of A-B trusts was limited by a 2011 amendment to the tax code that made estate tax exemptions “portable” between spouses. Under the new portability, a surviving spouse can claim the amount of any estate tax exemption not used by a decedent spouse by simply filing a form with the IRS. Then, upon the surviving spouse’s death, the effective exemption amount will be the survivor’s exemption, plus the unused portion of the first spouse’s exemption.

At first glance, this would seem to make A-B trusts irrelevant, particularly when combined with the recent dramatic increase in the estate tax exemption. However, some estate-planning attorneys have noted that, although taking full advantage of both spouses’ federal exemptions is the primary benefit of A-B trusts, it is not the only benefit. Of the states that have imposed estate taxes, only two (Hawaii and Maryland) had adopted exemption portability. And all of those states have substantially lower exemption amounts compared to the IRS.

For residents of Florida, where there is no state “death tax,” that’s less of a concern – unless a surviving spouse might move to a state with the tax. However, there are other situations in which an A-B Trust, or something similar, could still be useful. Perhaps most notably, an A-B trust can be used to ensure that a surviving spouse is fully provided for during life, but that the appropriate heirs ultimately inherit the estate in the appropriate amounts. That is, an A-B trust protects against, for example, a surviving spouse’s disinheriting the decedent spouse’s children from a prior marriage; or against attachment by the surviving spouse’s creditors; or against wasteful spending by the surviving spouse.

Further, while the gift and estate tax exemption is now portable, the GST exemption is not. So, if, for instance, a couple wants to leave substantial wealth to grandchildren – perhaps to avoid squandering by the intervening generation – an A-B trust may be necessary to gain maximum benefit of the GST exemption.

And, finally, when it comes to estate tax planning and A-B Trusts for high net worth estates,there’s the question of appreciating assets and inflation adjustment. An exemption transferred through portability is not indexed for inflation, and, if the surviving spouse outlives the decedent by an extended period, estate assets could appreciate substantially. If the decedent spouse’s exemption is applied at the time of death to assets held in a bypass trust, the wealth held in the trust will eventually transfer to the next generation free of estate tax regardless of how dramatically the value increases. But an exemption transferred through a portability claim might not be sufficient to cover the same assets by the time the surviving spouse dies.

On the other hand, appreciating investments receive a step-up in basis for estate planning purposes in Florida and elsewhere every time they pass through an estate. So, using portability to pass equities through the estates of both spouses could result in big income tax savings.

What it ultimately boils down to is that, although A-B trusts are not as widely relevant as they once were, under the right circumstances, they can still be a highly valuable estate-planning tool. An experienced estate-planning attorney can help you decide if an A-B trust is a good approach to take based on your financial situation and goals – and help craft an overall estate plan tailored to your priorities.

Steve Gibbs, Esq.

Great Article!

You must log in to post a comment. Log in now.